The landscape of environmental concerns confronting business owners has evolved significantly over the decades, beginning with the concept of corporate social responsibility in the 1950s, the triple bottom line framework which includes the three P’s of sustainability (people, planet and profit) in the 1990s, and most recently, the emergence of environmental social governance (ESG). These evolving agendas can be confusing, but a fundamental truth persists: Business owners must be diligent and proactive in addressing environmental risks. Creating an environmental risk management strategy for your business starts with a two-pronged approach:

- Training employees to identify and mitigate potential environmental pollution risks.

- Understanding environmental liability, including the coverages you may or may not have with your business insurance.

Pollution Prevention Practices

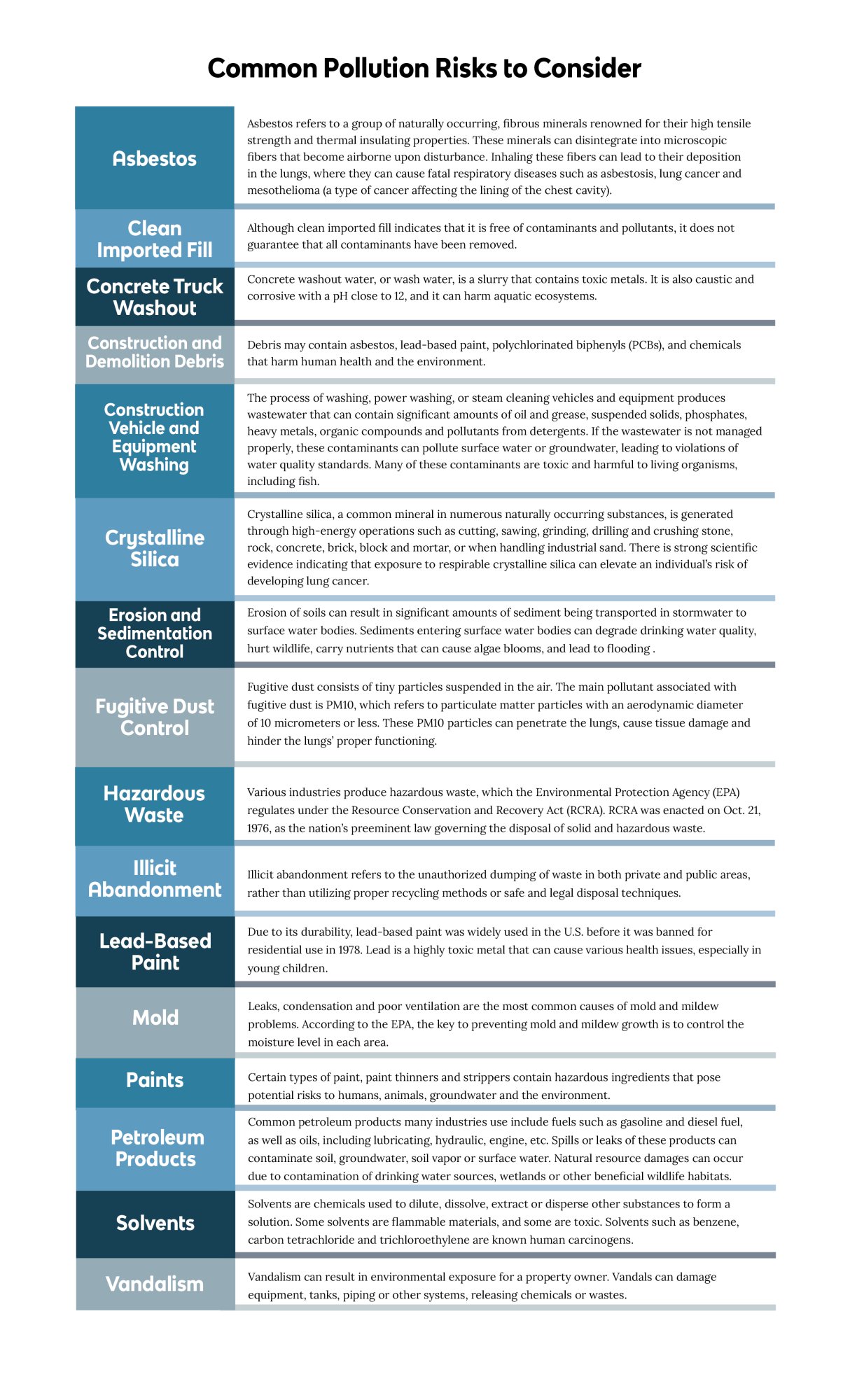

It is important to note that environmental exposures extend beyond businesses engaged in abatement, restoration and remediation activities. Site-based work is one of the most environmentally hazardous settings within the construction sector. Therefore, your team’s safety training program should include procedures for identifying potential pollutants encountered on a jobsite, including those brought in by the crew and those transported off-site for disposal. Figure 1, includes common pollution risks to consider.

Establishing protocols for your employees can help prevent accidents from happening. In addition to the exposures in Figure 1, it is best practice to have procedures for the following:

- Cargo securement

- Good housekeeping

- Loading and unloading

- Responding to spills

- Stockpile management

- Stormwater management

- Solid waste management

- Subcontractor vetting

- Utility locating

Contractors Pollution Liability

Historically, insurance advisors have not extensively addressed environmental risks with their construction clients. This lack of thorough discussion has led many companies to mistakenly believe that their operations are not at risk from environmental hazards. Consequently, contractors may be putting their businesses at risk. Although pollution claims are relatively infrequent, the severity of them can bankrupt a company.

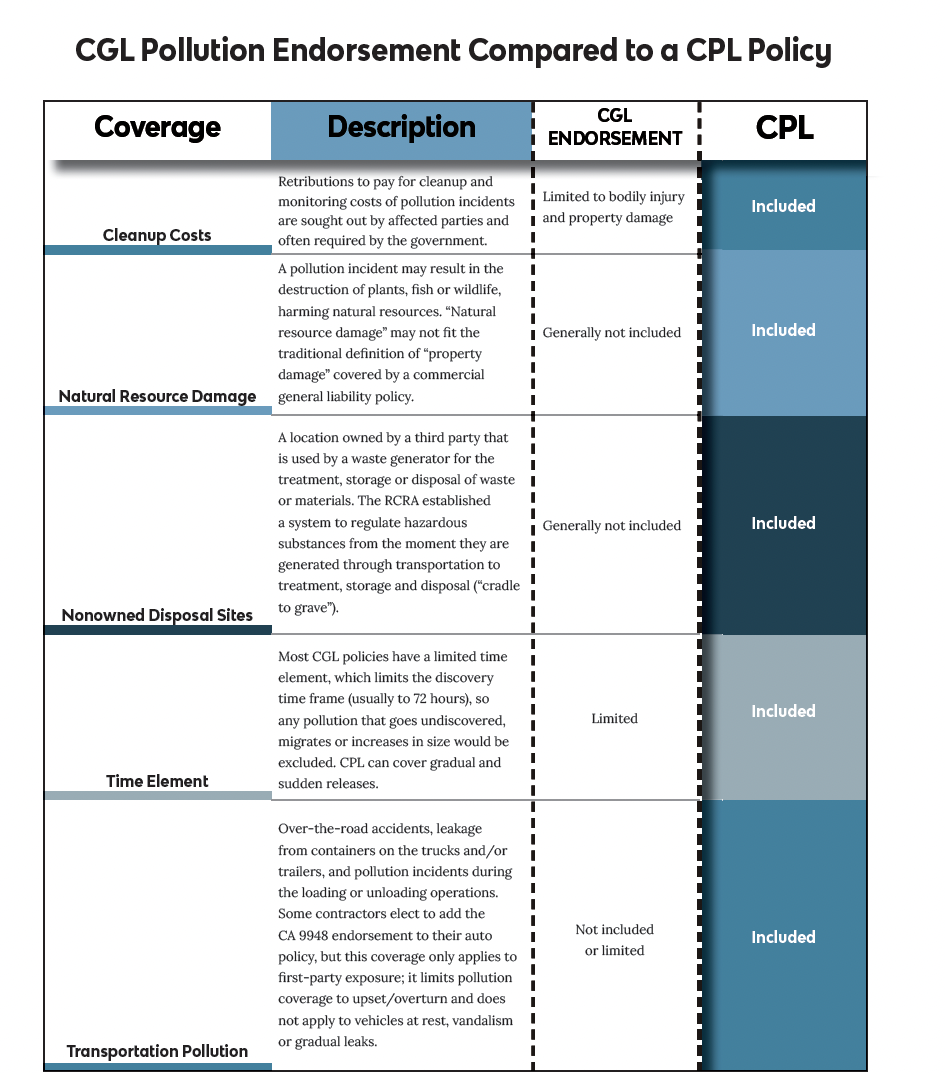

Commercial general liability (CGL) insurance carriers began introducing exclusions on pollution incidents in the 1970s. They started with a “sudden and accidental exclusion,” then moved to the “absolute pollution exclusion” in the 1980s, and the “total pollution exclusion” in the 1990s, which remains today. Some carriers offer givebacks for pollution coverage with an endorsement; however, those givebacks typically only provide bodily injury or property damage resulting from a pollution event. Most pollution claims also include extensive cleanup, as well as transportation or disposal expenses, which wouldn’t be covered.

It is also important to note that CGL policies are capped at a specific limit, representing the maximum amount the policy will cover on behalf of the insured. Should a contractor opt to add a pollution endorsement to their CGL policy, the coverage limits are often shared with the CGL policy. Any other claims would reduce what is available for a pollution claim.

A separate contractors pollution liability (CPL) policy provides comprehensive coverage for third-party bodily injury, property damage, defense expenses and cleanup costs associated with pollution incidents that arise from covered contracting operations. Figure 2 compares a CGL pollution endorsement and CPL policy.

Procurement & Subcontractor Vetting

Hiring clients rely on certificates of insurance to verify that contractors have active insurance policies. Unfortunately, the information provided in the majority of certificates of insurance falls short when it comes to pollution insurance. Standardized certificates like the Association for Cooperative Operations Research and Development (ACORD) forms were established in the 1970s; it is nearly impossible to determine from an ACORD what type of pollution coverage is available. Therefore, it is crucial to thoroughly screen contracts and subcontractors to prevent bearing the costs of a potential pollution event.