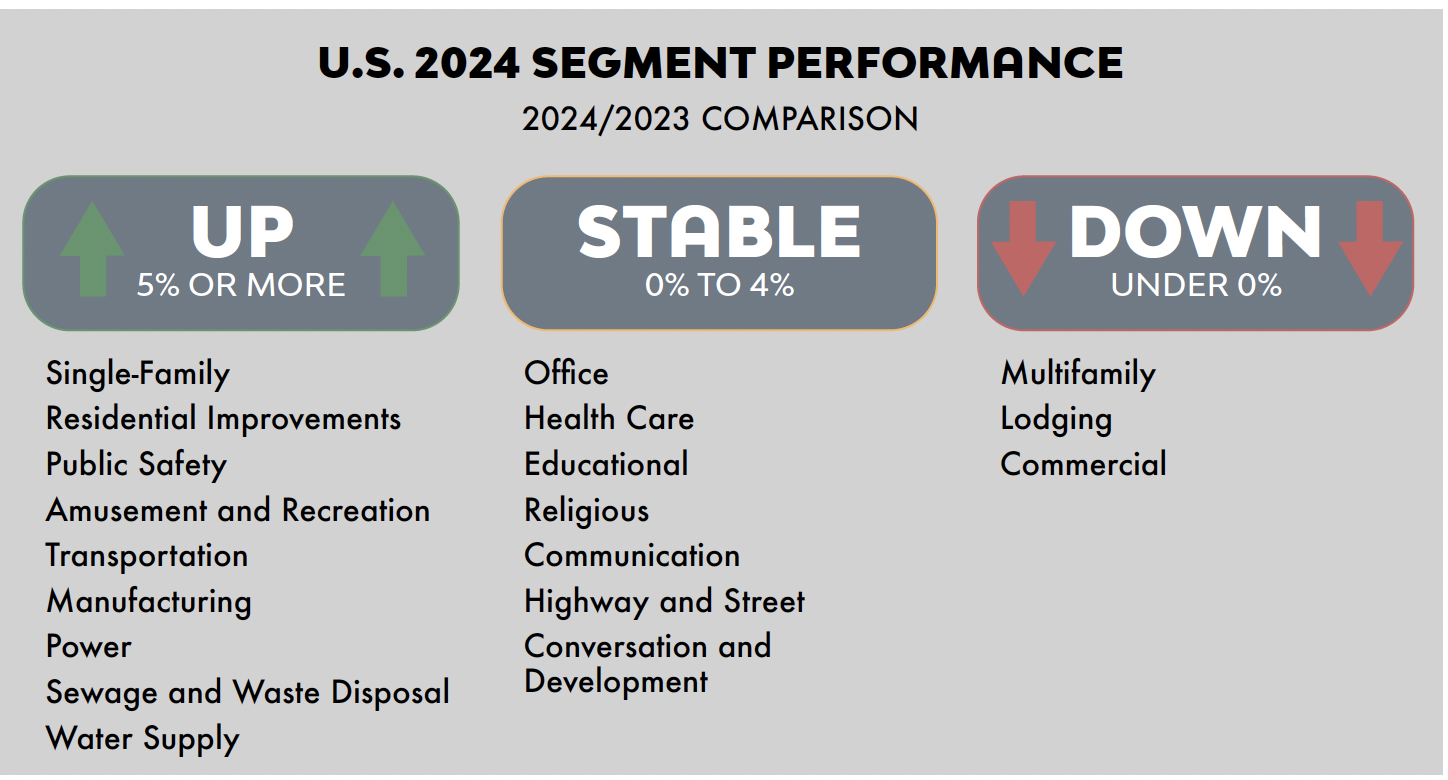

In what appears to be a continuation of the previous year’s performance, the construction industry continued to see either growth or stability in all its sectors in 2024. Anchored by a large thrust in the residential sector once again, businesses largely flourished. Most organizations have seen stability in both profitability and the competitive landscape, according to FMI’s Civil Infrastructure Index. Below (Figure 1) is an excerpt from FMI’s last quarterly outlook of 2024, illustrating the market sector perspective.

In a sizable juxtaposition to the industry’s performance, there are also lingering signs of troubled waters for all businesses. For instance, within that final snapshot, FMI’s predictive indicators of a potential recessionary market, flagged in four of the five core categories. The yield curve inversion, unemployment rate, new home sales and the overall supply of new homes were the troubling signs of a potential recessionary market. The one bright side was a positive change in year-over-year residential construction employment, which showed strength. By no means is this to say we are in a recession nor are we necessarily headed for one, but business leaders would be wise to remain vigilant and strategically focused in 2025.

With cautious optimism, contractors largely appear to be creating backlog faster than they are burning it. There are several trends that appear to be on the forefront of everyone’s mind leading into this year. Some appear to be extensions of themes that have persisted for several years, either through a continued evolution of those themes or a general lack viable solutions.

Dramatic Changes in the Digital World

One of the largest themes remains the increase of digital solutions in the market and the need to capitalize on artificial intelligence (AI) with an appropriate strategy. Every industry is continuing to investigate avenues to leverage AI to improve every aspect of their business. Construction leaders are similarly trying to find the angle, balancing an industry heavily predicated on human capital and equipment all while integrating the correct tools. Technology firms are moving at an exponential rate to provide sophisticated applications, while constructors appear saturated with options as they navigate the most cost-effective solution to improve productivity, drive utilization, increase bid accuracy, enhance safety, improve quality assurance/control and, ultimately, reduce risk. More importantly, firms have created a higher level of integration between what has been traditional “information technology” and “operations.” Put another way, there is a strategic push to have a leader within the realm of technology work arm-in-arm with all facets of the business versus the traditional support role.

Continued Talent Woes & the Proactive Push

In what seems to be a continued theme for the last decade, if not longer, is the constant refrain of the shortage of qualified associates, both tradespeople and management. However, the greatest difference from previous iterations of this statement is the push toward creating a solution. For years, leaders have lamented the lack of workers, only to realize that the solution may be an easier solve than previously thought: Become an employer of choice. This does not mean there will be a massive surge in the supply of workers, but rather a focused cultivation of talent within the four walls of a business. The most progressive organizations have created a strategy that focuses on onboarding, employee development, training, career progression and principles that retain top talent. Ultimately, the firms that focus on creating an employee-rich culture are able to leverage said culture more effectively. In the end, creating and developing talent begets more talent.

Surge in Strategic Growth

According to FMI’s fourth quarter Civil Infrastructure Index, 94% of the survey respondents indicated that their organizations had plans for expansion. The majority appear poised to grow organically while a small portion will utilize mergers and acquisitions. Whether this includes the expansion of current firm capabilities or some horizontal or vertical expansion, there is connective tissue between the firm’s talent strategy and this growth vector. A firm that adds a new division or department will need appropriate leadership. If this person comes from within, the firm is now responsible for finding an adequate replacement in order for the growth to make practical and profitable sense. Additionally, this push across the construction landscape could create a new host of competition issues. As stated previously, there appeared to be stability in the competitive ranks. Does 2025 create an influx of new strategic issues as companies add new “game pieces” to the board that previously did not exist?

Risk Management

Construction still remains one of the riskiest industries in the world. For years, firms have capitalized on risk management and even risk absorption to generate higher margins. However, the context around risk continues to be a sizable element that creates anxiety for firm leaders. Risks such as cybersecurity have become such commonplace for every industry that failure to create mitigation strategies is unacceptable. Full comprehension of risk management in finance, safety, technology, contract law and human capital is required and no longer the role of one person ensuring there is the appropriate policy coverage.

The Rise of the Machines

While it seems redundant to discuss technology twice, the same thrust in the technology arena is one of the growth engines. Previously, there was the push in electric vehicles, battery production and large-scale charging stations. While still prevalent, the same fervor lies in data centers and the need to create complementary and scalable solutions to the nation’s technological infrastructure needs. In some cases, the push to build such facilities creates a sizable burden on the labor market simultaneously. For example, consider the labor needs to construct a $30 billion data center in a midsize market. Now consider the ramifications of finding labor if you are not involved in the construction of said data center. Ancillary businesses see a boon in growth, which is welcome, while also creating an added wrinkle in the competitive landscape.

The “megatrends” that are the cornerstones of 2025 would be incomplete with adding a high level of uncertainty. As a new administration takes over, there are questions about immigration reform and its impact on the labor market. Additionally, there remain persistent concerns about macroeconomic landscape and how world markets will react to continued global strife.

These disrupters have manifested in the short term, wreaking havoc in logistics and supply chains in recent years. It appears that as one string is pulled, there is a domino effect of changes that leaders must consider. There certainly is optimism about 2025, but success will be achieved through careful and strategic actions.